Thinking About a 15-Year Mortgage? Read This First

If you’ve been shopping around for a home loan, chances are you’ve come across the popular advice: opt for a 15-year mortgage if you want to save big on interest. It’s a tempting proposition: lower rates and a faster payoff? Who wouldn’t want that?

But like most things in personal finance, the smartest move often lies beneath the surface. The truth is, a 15-year mortgage isn’t the right answer for everyone, and locking yourself into higher payments could put your future financial stability at risk.

Let’s break down the real story and explore a flexible alternative that could give you the best of both worlds.

The Allure of the 15-Year Mortgage

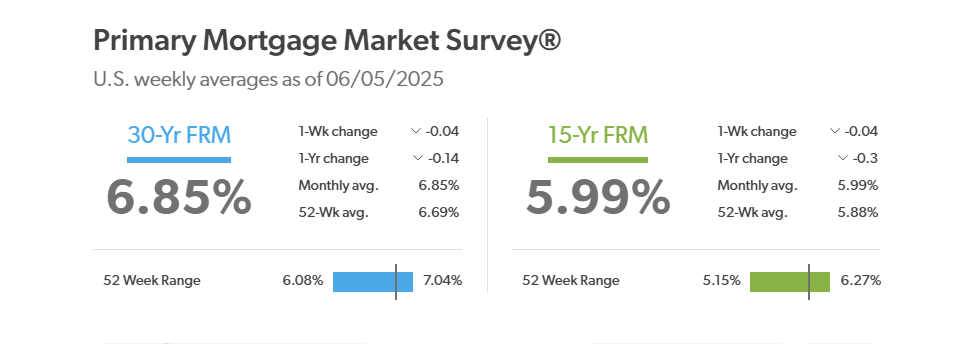

There’s no question that lenders typically offer lower interest rates on 15-year mortgages compared to 30-year ones. According to recent data from Freddie Mac, the average interest rate on a 15-year fixed mortgage (6.85%) can be up to 12% lower than its 30-year counterpart (5.88%). That adds up to significant interest savings over the life of the loan.

You’ll also pay off your home twice as fast, which can bring peace of mind and unlock long-term financial freedom. For homeowners nearing retirement or those who simply want to own their home outright sooner, that’s a powerful motivator.

But here’s the catch: those benefits come with a tradeoff.

The Bigger Monthly Burden

When you cut your mortgage term in half, your monthly payments don’t just increase slightly: they can jump substantially. For example, on a $300,000 loan, a 30-year mortgage might run around $2,000 a month, while a 15-year version could push you closer to $3,000 ( depending on rates and taxes).

That’s a pretty big difference. And while it might feel manageable today, what happens if you hit a financial bump in the road, like a job loss, medical emergency, or sudden home repair?

With a 15-year mortgage, you’re locked into those higher payments. There’s no wiggle room unless you refinance, which comes with its own costs and risks.

A Smarter Strategy: Flex Your 30-Year Like It’s a 15

So, how do you enjoy the benefits of a 15-year mortgage without being handcuffed to the high monthly payments? Here’s the pro move: Take out a 30-year mortgage, but pay it down as if it were a 15-year loan.

In practice, that might mean:

- Adding an extra $500 to $1,000 to your monthly principal payment

- Making biweekly payments instead of monthly ones

- Using annual windfalls (bonuses, tax returns) to make lump-sum payments

This strategy allows you to pay off your loan faster and save on interest while retaining flexibility if your finances ever take a hit. If life throws you a curveball, you can simply fall back on your required 30-year payment amount without penalties or pressure.

Why This Approach Works Especially Well for Georgia Homeowners

In a housing market like Atlanta, where home prices and property taxes can vary widely by neighborhood, this approach can be a gamechanger. It gives first-time buyers or growing families the ability to enter the market with a safety net, while still making meaningful progress on their mortgage.

It also aligns with smart financial planning: emergency savings, retirement contributions, and debt reduction shouldn’t be sacrificed just to knock a few years off your mortgage.

By choosing flexibility now, you’re protecting your future self from financial stress while still making aggressive headway on homeownership.

Bottom Line: It’s Not Just About the Rate

Yes, 15-year mortgages offer lower interest rates. But the “best” mortgage isn’t just about the numbers, it’s about how it fits into your full financial picture.

Before signing on the dotted line, ask yourself:

- Can I truly afford the higher monthly payments without stress?

- Am I prioritizing other important goals like saving and investing?

- Do I want the flexibility to adjust my payments in the future?

For many, a 30-year mortgage with an accelerated payoff plan checks all the boxes: it offers savings, freedom, and peace of mind.

In the end, it’s not about paying the mortgage off fastest, it’s about paying it off smartest.