Social media has become a go-to place for financial advice. From budgeting tips to debt payoff strategies, influencers promise shortcuts that sound smarter and faster than traditional money management. When it comes to credit, those promises can feel especially tempting.

But the Federal Trade Commission is warning consumers about a growing viral trend that crosses from bad advice into criminal behavior. Influencers are encouraging people to file false identity theft reports to remove legitimate debts. The result, as you can imagine, can be disastrous. Beyond the significant damage to your credit score, we’re talking real-life legal consequences and extensive financial harm.

How the Credit Report Scam Works

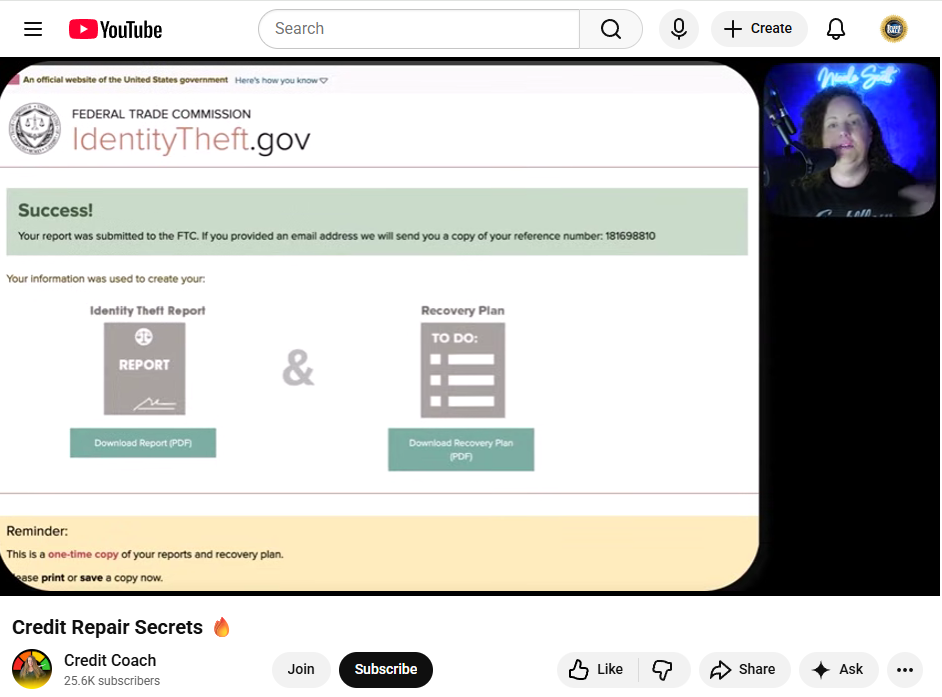

The scheme is often framed as a clever loophole. Influencers tell followers that if they report a debt as identity theft, credit bureaus will automatically remove it from their credit reports. Some videos claim the process is guaranteed, fast (“within four days!”), and completely legal.

In reality… y’all, filing a false identity theft report is a crime. When someone submits an identity theft affidavit or police report for a debt they actually owe, they are making a false statement. That’s fraud, and it can lead to fines, criminal charges, and even jail time. It can also flag a consumer as untrustworthy, which will absolutely destroy any chance of a positive resolution for any actual disputes in the future.

The FTC has been clear that no credit repair company or individual can legally remove accurate and current information from a credit report. If a debt is real, it belongs there until it ages off or is resolved.

How Influencers Are Promoting the Scam

Many of these influencers position themselves as “financial coaches” who discovered the ultimate Financial Cheat Code (“the one financial trick credit bureaus hope you never find out!” – puh-leez). The associated content often includes screenshots of temporary credit score changes, testimonials from followers, or step-by-step scripts that appear official.

The motivation, of course, is profit-driven. Some influencers sell templates, classes, or private coaching sessions that walk consumers through filing false reports. Others earn revenue through affiliate links tied to credit monitoring services or paid communities. The more spectacular the claim, the more engagement the content receives.

This creates a cycle where misleading advice spreads faster than accurate information. Algorithms reward drama, not accuracy (read that again).

Why This Advice Keeps Spreading

Credit stress is universally the worst, and it makes people vulnerable. For some, it may seem like an obvious trap that people naively stroll right into. But that’s not usually the case. Think about it: when somebody is struggling to qualify for a loan, rent an apartment, or lower their interest rates, a quick fix can feel worth the risk. Bad-faith influencers like these target terrified people, not stupid people.

General confusion around legitimate credit rights doesn’t help things. Point blank: consumers are allowed to dispute errors and report real identity theft. This scam is effective because it just blurs the truth, making it seem like strategic wording and confidence is all it takes to turn fraud into something legally acceptable.

What Consumers Can Do Instead

Thankfully, improving your credit doesn’t require breaking the law. There are safe, free steps consumers can take that actually work (over time).

- Check credit reports regularly for errors and unauthorized accounts

- Dispute inaccurate information directly with the credit bureaus

- Pay bills on time and reduce balances when possible

- Avoid anyone who promises guaranteed credit score increases

Consumers can learn more about legitimate credit repair options at ftc.gov/creditrepair. Everyone in the United States can also check their credit reports weekly for free from Equifax, Experian, and TransUnion at AnnualCreditReport.com.

You can read the FTC’s consumer alert about this scam here.

Final Thoughts

When something goes viral, from pop culture to politics to financial advice, it deserves a little extra scrutiny. If a tip sounds too easy, too fast, or too secretive, it is worth slowing down before acting. Credit decisions follow consumers for years, and one bad move can undo months of progress (or put you further in debt... or send you jail).

TrustDALE encourages consumers to rely on verified information and vetted professionals (it’s kind of our thing). Bottom line, if you need help navigating something as precarious and convoluted as credit, you should only trust advice from legitimate professionals who focus on long term solutions. Risky shortcuts rarely work out, and when it comes to your credit, they can cost you far more than they can ever save.